One of the primary monetary news items to note as 2010 draws to a close is the announcement of more ‘quantitative easing’ by the Federal Reserve1. In plain terms, this means that the Fed will purchase treasuries on the open market. This will have the effect of artificially increasing demand for treasuries, which will push down the rate of interest. It is also expected to have the effect of pushing more money out into the economy with the hopes that it will stimulate consumer demand. Unfortunately, many fear that it will also stimulate inflation.

One of the primary monetary news items to note as 2010 draws to a close is the announcement of more ‘quantitative easing’ by the Federal Reserve1. In plain terms, this means that the Fed will purchase treasuries on the open market. This will have the effect of artificially increasing demand for treasuries, which will push down the rate of interest. It is also expected to have the effect of pushing more money out into the economy with the hopes that it will stimulate consumer demand. Unfortunately, many fear that it will also stimulate inflation.

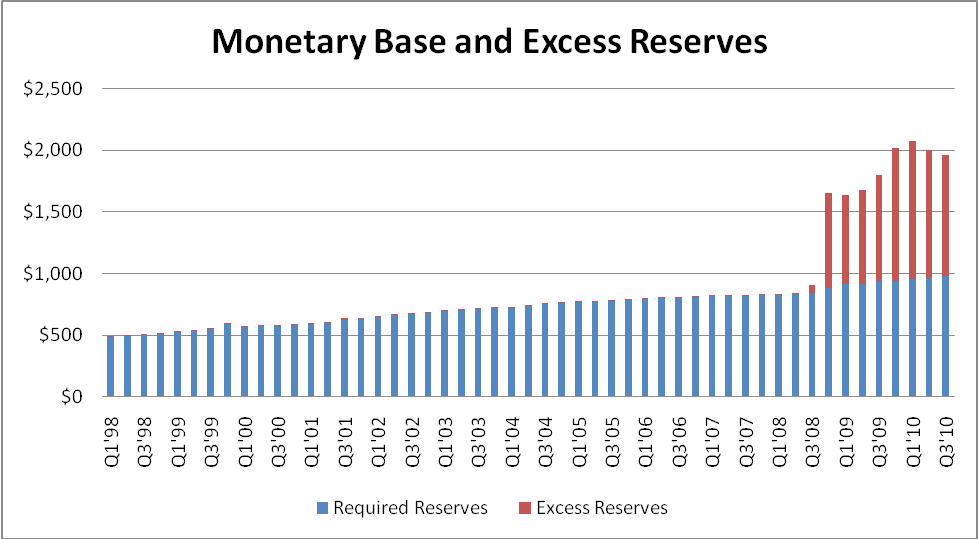

One of the most powerful tools that the Federal Reserve has in its arsenal is the rate it charges member banks for loaned funds. (Also known as the “Fed Funds” rate) In the aftermath of the 2008 financial crisis, the Fed Funds rate lowered to just a few basis points. (Effectively Zero) The effect of this move was to immediately flood the balance sheets of banks with liquidity. This also created a vast sea of un-loaned reserves on the balance sheets of banks.

In a normal lending environment, capital at the bank is lent out at a 10 to 1 ratio so that the bank can earn interest on the loaned funds. In the current environment, banks can borrow money from the Fed at near-zero interest rates, and many are earning profits by churning borrowed funds into treasuries to profit from the yield spread between the treasuries and the rates charged by the Federal Reserve. The fundamental problem is that the nearly $1 Trillion in un-loaned reserves can literally be turned into new loans overnight. This could potentially mean the addition of up to $10 trillion in new money at any given time.

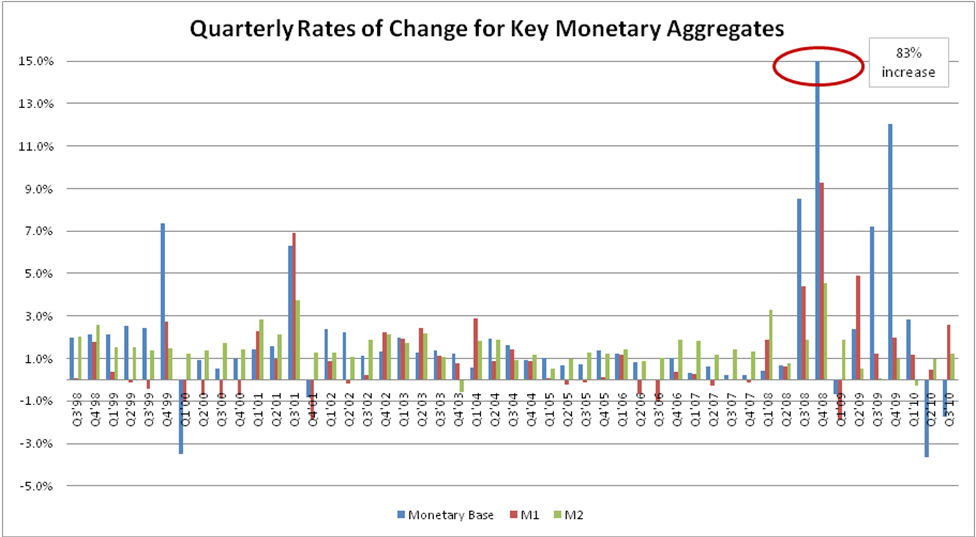

In practice, a flood of loans like this is quite unlikely. Analyzing the rates of change for key monetary aggregates reveals that the M1 and M2 measurements have grown much more slowly than the Monetary Base2, even when accounting for the massive increase following the 2008 financial crisis. The way that this expansion of money has been held out of broad circulation is by government sponsored treasury arbitrage from artificially low interest rates from the Federal Reserve. As we move into 2011, the principal monetary question facing investors is that of whether the Fed will decide to increase its Fed Funds rate, shifting incentives for banks to stop arbitraging treasuries and resume making loans. When this ultimately happens, it will create broad and rapid price escalations. Our models indicate that the current administration will use all of the tools in its disposal to delay this phenomenon in an attempt to create the appearance of economic recovery in advance of the 2012 election cycle.

In practice, a flood of loans like this is quite unlikely. Analyzing the rates of change for key monetary aggregates reveals that the M1 and M2 measurements have grown much more slowly than the Monetary Base2, even when accounting for the massive increase following the 2008 financial crisis. The way that this expansion of money has been held out of broad circulation is by government sponsored treasury arbitrage from artificially low interest rates from the Federal Reserve. As we move into 2011, the principal monetary question facing investors is that of whether the Fed will decide to increase its Fed Funds rate, shifting incentives for banks to stop arbitraging treasuries and resume making loans. When this ultimately happens, it will create broad and rapid price escalations. Our models indicate that the current administration will use all of the tools in its disposal to delay this phenomenon in an attempt to create the appearance of economic recovery in advance of the 2012 election cycle.

* Don’t forget that The Masters of Income Property Investing educational event takes place this March 4-6, 2011, which is coming up very soon. You can buy your tickets at an almost 50% discount for a few more days, but we’d suggest you visit JasonHartman.com now before all seats are gone.

The Solomon Success Team

![]()

Flickr / DonkeyHotey